The desire for homeownership burns bright in Virginia. With its rich history, vibrant cities, and stunning natural landscapes, the state offers a captivating lifestyle for many. But what if your credit score isn’t sparkling? Fear not, Virginians with less-than-perfect credit! This guide explores practical steps to navigate the path toward homeownership in the Commonwealth.

Understanding Credit and the Virginia Landscape

Obtaining a mortgage hinges on your creditworthiness, a measure of your past borrowing behavior. FICO scores, typically ranging from 300 to 850, are the most commonly used credit rating system. In Virginia, as elsewhere, a higher credit score translates to more favorable loan options with lower interest rates.

Learn more about Credit Score here on Equifax.

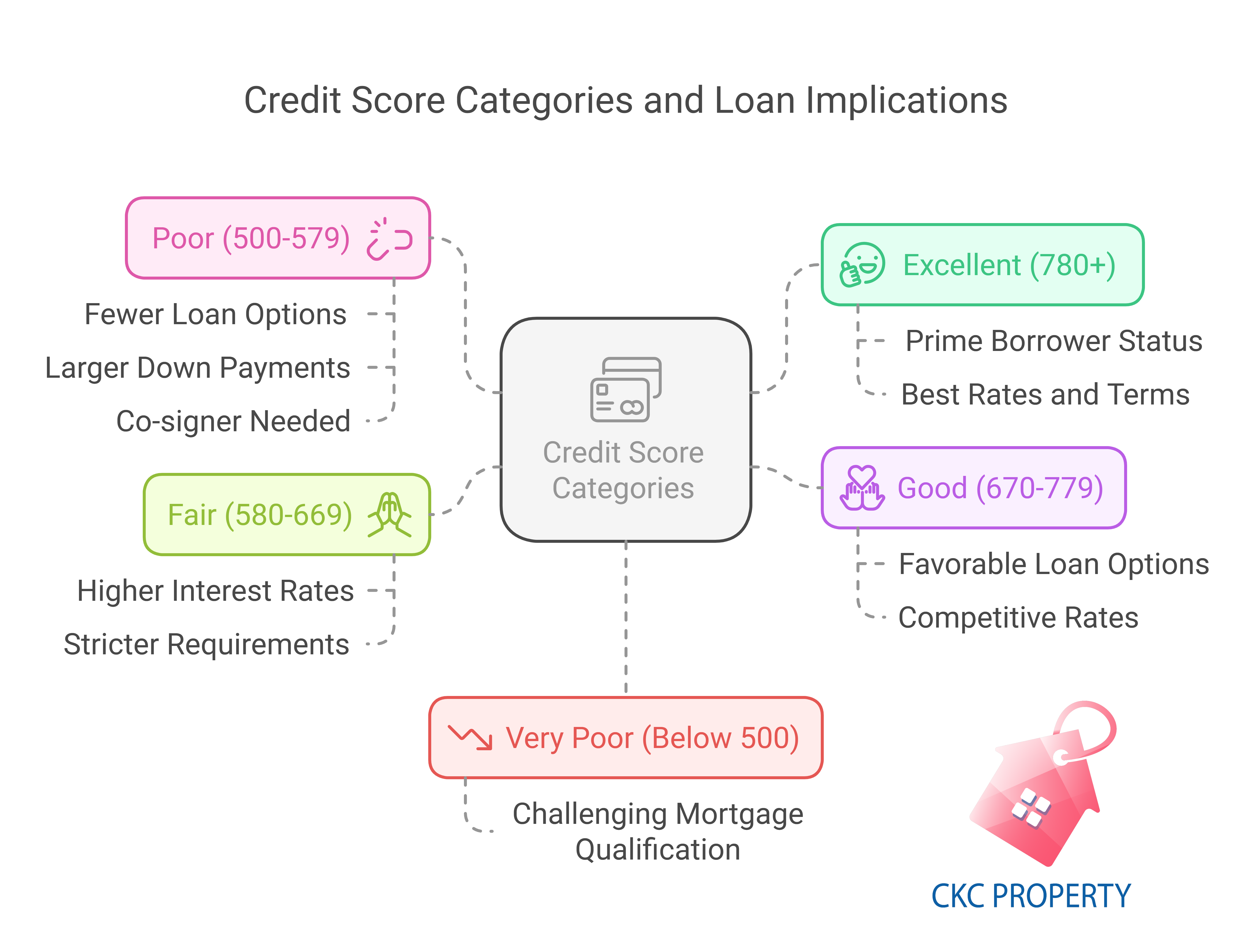

Here’s a breakdown of credit score ranges and their general mortgage implications:

Excellent (780+) – Prime borrower status, qualifying for the best rates and terms.

Good (670-779) – Favorable loan options with competitive rates.

Fair (580-669) – Loan options may be available but with potentially higher interest rates and stricter requirements.

Poor (500-579) – Fewer loan options, likely requiring larger down payments or a co-signer.

Very Poor (Below 500) – Qualifying for a mortgage becomes significantly more challenging.

Taking Charge: Strategies for Homeownership

Even with a less-than-ideal credit score, the dream of homeownership in Virginia remains achievable. Here are some proactive steps you can take:

Know Your Score and Credit Report: Obtain a free credit report from each of the three major credit bureaus (Equifax, Experian, and TransUnion) at https://www.annualcreditreport.com/index.action. Dispute any errors you find, as even minor inaccuracies can negatively impact your score.

It is the only website the federal government authorizes to provide free annual credit reports.

Another option is to access your credit report directly from the credit bureaus for a small fee.

Credit Score Improvement: Implement strategies to raise your credit score. Timely bill payments, responsible credit card utilization (ideally below 30% of your limit), and maintaining a healthy mix of credit card and installment loan accounts can all contribute positively.

Save for a Down Payment: A larger down payment demonstrates financial commitment and reduces the loan amount needed. Aim for at least 3.5% for FHA loans (government-backed loans with more lenient credit score requirements) and 20% for conventional loans (typically offering lower interest rates).

Affordability Check: You can use free online calculators, like the one provided by Veterans United, to check if you can afford a home loan based on your current income. This tool helps you estimate how much home you can afford.

Same way there are multiple free calculators available for different purposes, such as Mortgage Payment, Refinance, Funding Fee, Basic Housing Allowance, Loan Limit, etc

Credit Score and Mortgage Landscape:

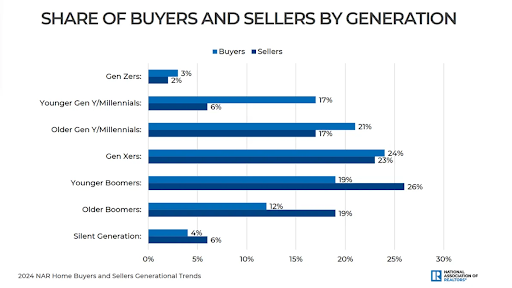

National Association of Realtors (NAR): The NAR publishes an annual “Home Buyer and Seller Generational Trends Report” which often includes infographics on credit score distribution amongst homebuyers.

The graph below illustrates home transactions across the USA by generation. These statistics are sourced from the National Association of Realtors.

Source: Nar.realtor

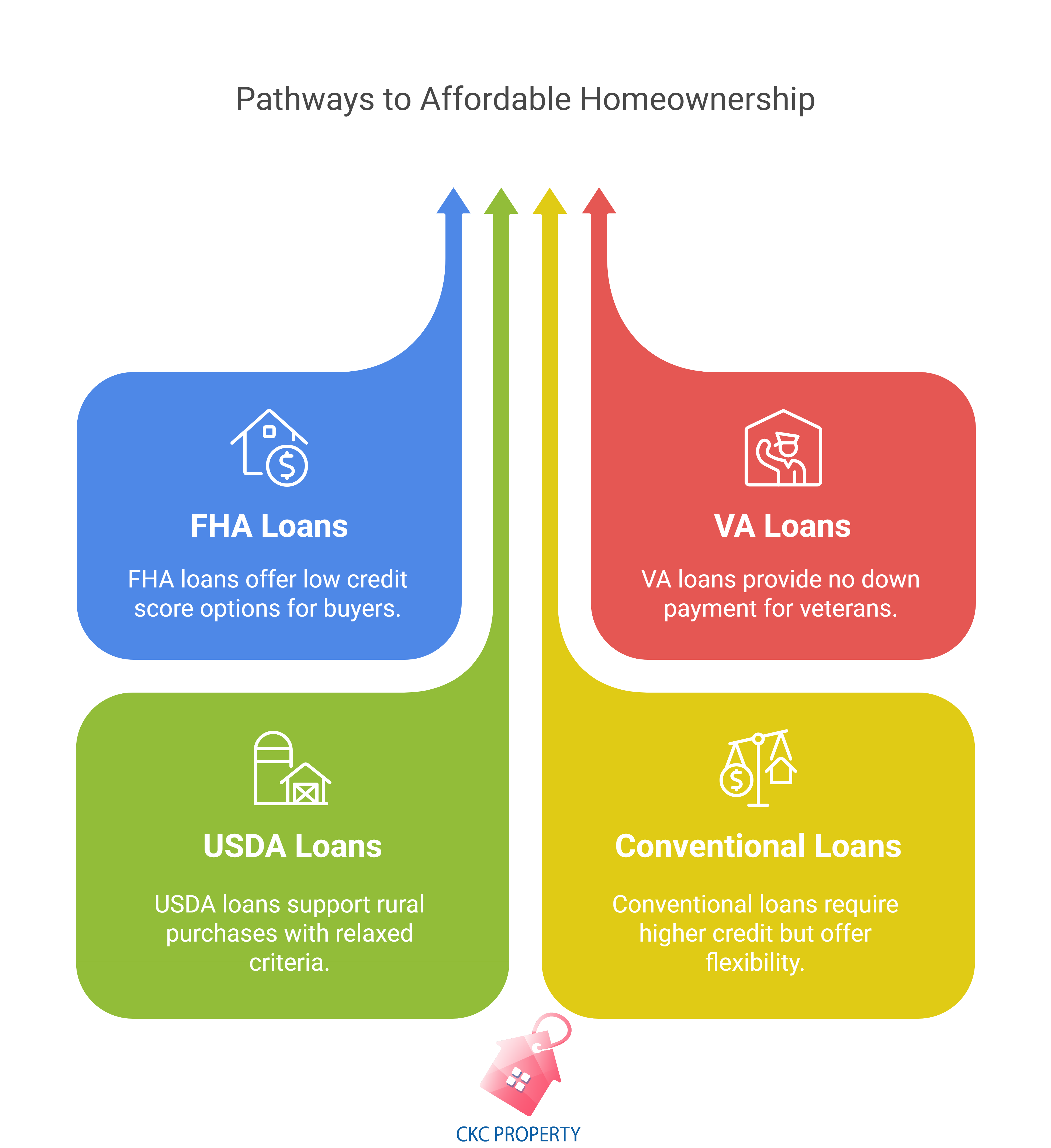

Loan Options for Virginians with Lower Credit Scores

While traditional lenders may be hesitant with lower credit scores, several loan options cater to borrowers in your situation:

While traditional lenders may be hesitant with lower credit scores, several loan options cater to borrowers in your situation:

FHA Loans: Backed by the Federal Housing Administration, these loans allow for lower minimum credit scores (as low as 580 with a 10% down payment or 500 with a 3.5% down payment). This government-backed loan especially benefits first-time home buyers.

On the HUD.GOV website, you can find more information.

VA Loans: For eligible veterans and active-duty service members, VA loans require no down payment and offer competitive interest rates. The Department of Veterans Affairs backs it and it provides VA Loans for eligible veterans, active-duty service members, and their better halves.

You can find more information on this on the VA.GOV website

USDA Loans: The United States Department of Agriculture offers loans for rural property purchases with relaxed credit score requirements.

More information can be found on the website https://www.rd.usda.gov/va

Conventional Loans: A conventional loan is a type of mortgage that isn’t insured or guaranteed by the government. Instead, it follows guidelines set by Fannie Mae and Freddie Mac and can be bought or sold on a secondary market. These loans can have fixed or adjustable interest rates and can cover up to 97% of the home’s value. If you borrow more than 80% of the home’s value, you may need to pay for mortgage insurance, either yourself or through the lender.

Additional Considerations: Finding the Right Partner

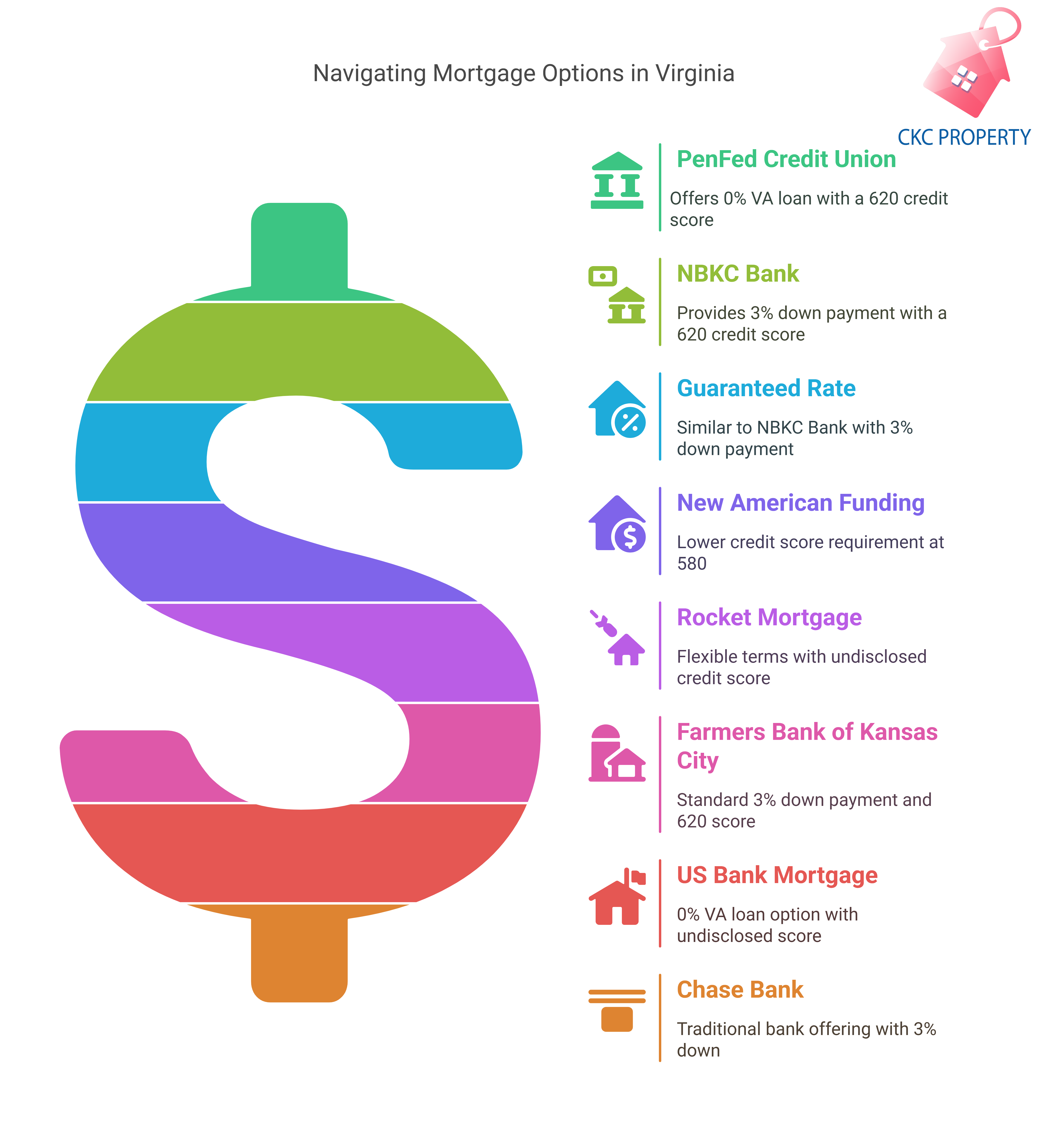

Mortgage Lender: Shop around and compare rates from various lenders, including banks, credit unions, and online lenders. Look for lenders specializing in bad credit mortgages.

Lender | US News Rating | Minimum Down Payment | Minimum Credit Score |

PenFed Credit Union | 4.8% | 0% of VA Loan | 620 |

NBKC Bank | 4.8% | 3% | 620 |

Guaranteed Rate | 4.8% | 3% | 620 |

New American Funding | 4.7% | 3% | 580 |

Rocket Mortgage | 4.7% | 1% | Not Disclosed |

Farmers Bank of Kansas City | 4.7% | 3% | 620 |

US Bank Mortgage | 4.7% | 0% of VA Loan | Not Disclosed |

Chase Bank | 4.6% | 3% | Not Disclosed |

Veterans United Homes Loans | 4.4% | 0% of VA Loan | 620 |

PNC Bank | 4.3% | 3% | 620 |

Real Estate Agent: An experienced real estate agent can guide you through the home-buying process, negotiate offers, and connect you with resources tailored to your situation.

CKC Property: Your Trusted Partner in Virginia Real Estate

At CKC Property, located in Richmond, Virginia, we understand that the path to homeownership can be unique for everyone. We offer comprehensive services to guide Virginians through the buying process, whether you have stellar or less-than-perfect credit.

Our team can assist with:

Credit Repair and Building: Through our affiliated company, CKC Solutions, we provide credit counseling and strategies to improve your credit score.

Pre-Approval: Getting pre-approved for a mortgage clarifies your budget and strengthens your offer when making bids on properties.

Finding the Right Property: Our experienced real estate agents will work diligently to find a house that aligns with your needs and budget.

Negotiation and Closing: We’ll guide you through offer negotiations and ensure a smooth closing process.

Beyond Credit: Additional Resources for Virginians

Virginia offers programs and organizations dedicated to helping aspiring homeowners:

Virginia Housing: This state agency provides down payment and closing cost assistance programs for eligible homebuyers (https://www.virginiahousing.com/en).

NeighborWorks America: This national non-profit offers resources and financial assistance programs for homeownership, including those specifically targeted towards individuals with lower credit scores (https://neighborworks.org/home).

Facing Foreclosure? There’s Help Available

If you’re facing foreclosure on your current Virginia property, don’t lose hope. Several resources can help you navigate this challenging situation:

Pre-Foreclosure Assistance: CKC Property offers pre-foreclosure assistance. Our team can connect you with legal and financial guidance to explore options such as loan modification, short sale, or deed-in-lieu of foreclosure.

Virginia Housing Counseling Coalition: This non-profit organization provides free foreclosure counseling services to Virginia homeowners (https://vahousingcounselors.org/).

Beyond Buying: Additional Services from CKC Property

We offer a comprehensive suite of services beyond buying a home:

Vacant Property Acquisition: Looking to invest in a rental property? We can assist with identifying and acquiring suitable vacant properties.

Distressed Property Purchase: We have extensive experience evaluating and purchasing distressed properties, offering win-win solutions for both sellers and investors.

Tax Lien Resolution: Facing tax liens on your property? CKC Property can guide you through the tax lien resolution process to protect your ownership.

Property Management: Once you become a homeowner or real estate investor, CKC Property can manage your property, ensuring smooth tenant relations and rental income collection.

Conclusion: The dream of homeownership in Virginia is within reach, even with credit challenges. By taking proactive steps, utilizing available resources, and partnering with an experienced team like CKC Property, you can navigate the path to owning your dream home in the Commonwealth.

Contact CKC Property Today!

We invite you to contact CKC Property today for a free consultation. Our team of experts is dedicated to helping you achieve your real estate goals in Virginia.

Additional Resources:

CKC Property Website: ckcbuyshomes.com

CKC Home Inspection: ckchomeinspection.com

CKC Solutions: ckcusinesspro.com

Disclaimer: The information provided in this blog post is for general informational purposes only and does not constitute financial or legal advice. Please consult with a qualified financial advisor or legal professional for personalized guidance.